How to measure output

In an economy, the following formula will always be true:

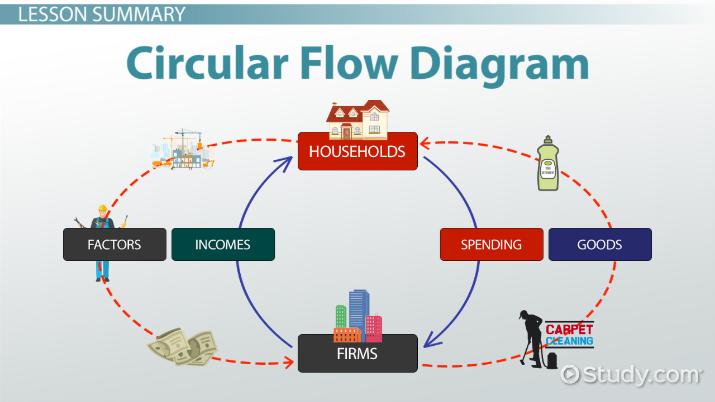

national output = national income = national expenditure

This is used to represent the circular flow of output, expenditure and income. This can be seen with a small example of an economy, which can consist of just three individuals: a candlemaker, a baker and a butcher. The butcher will buy candles from the candlestick maker, producing 10 dollars in expenditure and receiving a value of 10 dollars (the candles) in return, also called output. This same butcher will sell meat to other customers, such as the baker, who can pay 10 dollars for their meat (expenditure), for which the butcher will receive income (those 10 dollars). This can be seen in the following diagram:

Measuring economic activity

National output: The total value of output of goods and services produced in a macroeconomy.

National income: The total amount of income earned by factors of production in a macroeconomy.

National expenditure: What people and organisations spend on goods and services.

Gross domestic product (GDP)

The gross domestic product, also called GDP, is the total market value of all final goods and services produced within an economy by its factors of production in a given period of time. There are three main ways of measuring the GDP, which are: the output method, the income method, and the expenditure method. We will look at these in more detail in the following sections.

The output method

The output method consists of counting the value of all the output produced by firms in a specific period of time. To avoid a common problem known as double counting, which means counting the output twice by mistake and ending up with wrong figures, economists will only add up the value added by each firm at each stage of production. The gross value added (GVA) by each firm is the market value of its output of goods or services less the value of the inputs used in the production of its outputs.

The income method

The income method consists in counting the total income earned from the production of goods and services in an economy. In these calculations, transfer playments, such as welfare payments, unemploymment benefits, pensions, or any type of payment from a government to individuals, are excluded because they are unearned incomes, because nothing was being produced in order to earn that income.

The expenditure method

The expenditure method consists of the total value spent in goods and services in an economy. This includes spending by individual households, firms and government organisations. Spending on imported goods is excluded by spending on exported goods is counted. This is because exported goods have been produced by their own economy while imported have not.

Real vs. Nominal GDP

The main difference between real and nominal GDP is that nominal GDP is the money GDP, or the value of output, income and expenditure in an economy at their current market prices. Nominal GDP, therefore, does not actually measure how much purchasing power it equals, just the values at the current rates. On the other hand, real GDP measures changes in total output assuming prices are unchanged over time. In other words, the real GDP includes the amount of purchasing power you have, and takes into account the change in the value of the money.

A common mistake when looking at a nominal GDP graph is that some may think that there has been high growth, when in reality, it is just the value of the money increasing, but this is not always the case.

Governments and economists can use GDP statistics in several ways:

- A government can make better and more informed decision about the allocation of resources if they know how it is performing. For example, it can decise to invest more on capital goods and less on customer goods if the graphs show too high growth in customer goods and too low in capital goods.

- Standards of living can be compared throughout the years in the same country to see how they have developed.

- Standards of living can be compared with other countries or different areas of the same country.

Economic growth

Economic growth means there has been an increase in the real GDP of an economy. It can help to keep inflation low and stable. It is also a growth in the productive potential of an economy. It can be represented by showing a PPC (production possibility curve). In a PPC, economic growth can be seen as an outward shift in the curve:

How economies grow

An economy has several different ways of growing. They are listed below.

The discovery of more natural resources

If more natural resources are discovered, new labour opportunities will arise and therefore, there is more production pontential in the economy. This will have a large impact on economic growth. For example, when oil and gas were discovered, many countries grew rapidly as these resources were discovered and they still are. However, many countries lack the funds to be able to search for new natural resources, making this unlikely.

Investment in new capital and infrastructure

When firms invest in new capital and infrastructure, the production potential increases because now it might be either easier to produce goods and services or you could produce new goods and services which produce even more production potential to the economy. The government can help firms to invest in new capital and infrastructure by lowering the interest rates to make it more attractive for these firms to borrow money in order to do so.

Technical progress

New inventions can improve the production potential of an economy by allowing firms to produce goods and services at a faster and more efficient rate than before. They can also help to make new goods and services. An example of technical progress is fiberglass, which was originally designed as insulation material, and now is widely used from the production of bows to artificial limbs.

Increasing the amount and quality of human resources

A larger and more productive work force can boost economic growth. Education and training are often called "investments in human capital" and will help create a better skilled, knowledgeable and more productive workforce.

Reallocating resources

An inefficient allocation of resources will constrain economic growth. Moving resources from less-productive uses to more-productive uses will boost ouput and growth. Moving resources from the production of consumer goods and services into the production of capital goods will help increase the productive potential of an economy.

Comments

Post a Comment